Learn

You’re about to get the clearest picture available of what “August 2026 compliance” actually means in practice - which systems are affected, what’s required, what the penalties look like, and a realistic timeline for getting there.

Five months. That’s what you have.

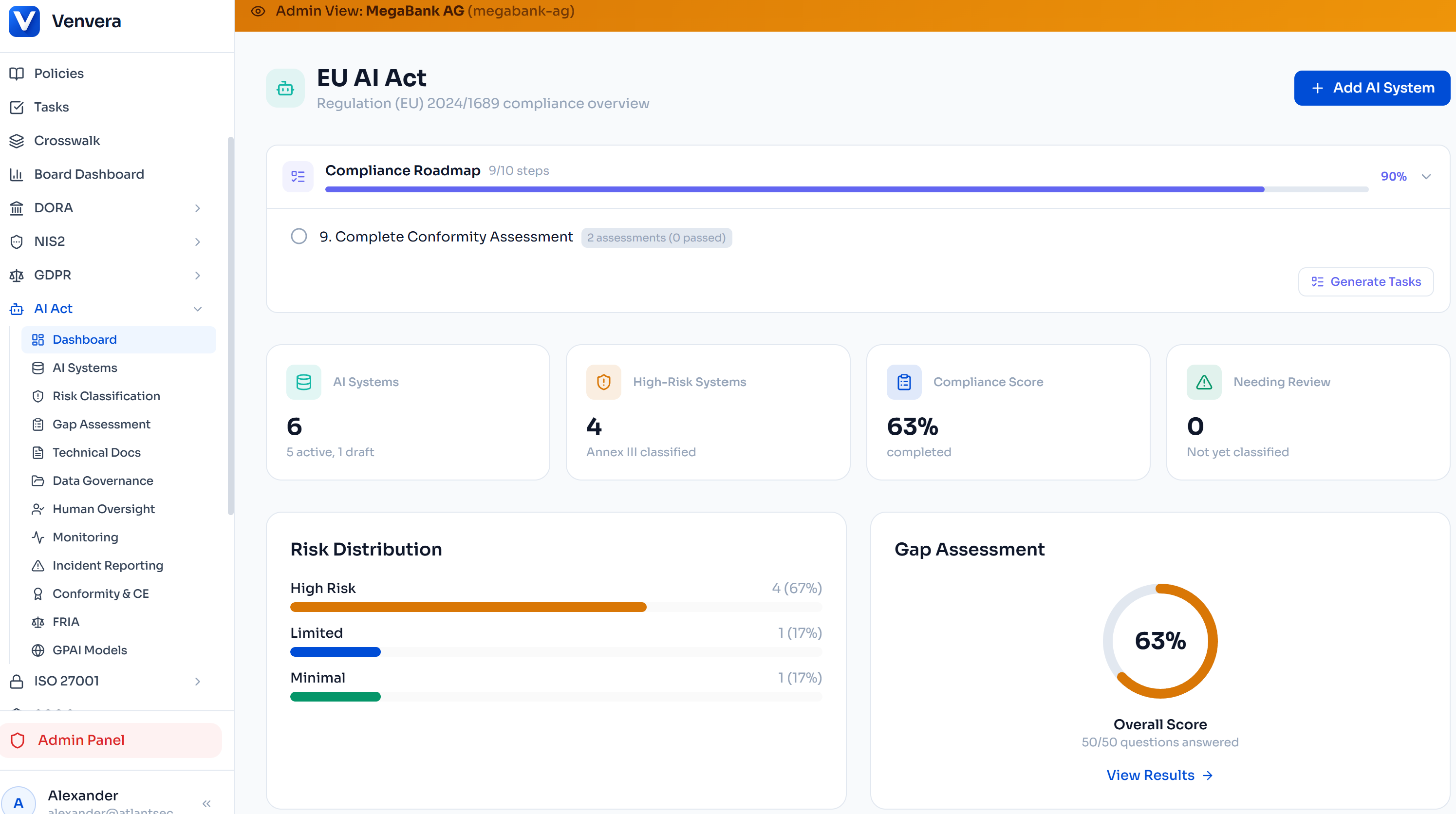

On 2 August 2026, the EU AI Act’s provisions for high-risk AI systems become fully enforceable. Financial institutions deploying AI for credit scoring, insurance pricing, risk assessment, or any other Annex III category will need to have conformity assessments completed, technical documentation in place, quality management systems operational, and systems registered in the EU database.

I keep hearing “we’re monitoring the situation” from compliance teams. Monitoring is what you do when a regulation is in draft. This regulation received Royal Assent - well, EU equivalent - in June 2024. The implementing timeline is set. August 2026 is not aspirational. It’s a hard deadline with penalties of up to €15 million or 3% of global annual turnover for non-compliance with high-risk provisions.

So let’s stop monitoring and start doing. Here’s exactly what that looks like.

The Full EU AI Act Implementation Timeline

The AI Act doesn’t go live all at once. It’s phased. Understanding the full timeline helps you see where August 2026 fits and what’s already in effect.

1 August 2024 - Entry into force

The regulation officially entered into force. The clock started.

2 February 2025 - Prohibited practices ban (ALREADY IN EFFECT)

AI practices deemed unacceptable are banned: social scoring, emotion recognition in workplaces/schools, real-time biometric identification in public spaces (with exceptions), manipulative AI. If you’re doing any of these, you’re already in violation.

2 August 2025 - General-purpose AI and governance provisions

GPAI model providers must comply with transparency obligations. National competent authorities must be designated. AI literacy obligations (Article 4) apply. Codes of practice for GPAI published.

2 August 2026 - HIGH-RISK AI SYSTEMS (YOUR DEADLINE)

All obligations for high-risk AI systems in Annex III become enforceable. Conformity assessments, technical documentation, QMS, registration, transparency, human oversight, data governance - all required. Financial services AI (credit scoring, insurance pricing) is Annex III.

2 August 2027 - Full application

Remaining provisions apply, including obligations for high-risk AI systems listed in Annex II (those regulated under existing EU product safety legislation).

What Exactly You Need by 2 August 2026

Let me be specific. On 2 August 2026, for every high-risk AI system you provide or deploy, you must have:

1. A completed conformity assessment

For providers: an internal assessment per Annex VI, or third-party assessment per Annex VII if biometric systems are involved. For deployers who have “substantially modified” a system: same requirement, because you’re now treated as a provider.

2. Technical documentation per Annex IV

Complete, current, and detailed enough for a market surveillance authority to assess your system without your help. This means architecture descriptions, training data documentation, test results, performance metrics, risk mitigation measures, and human oversight procedures.

3. A quality management system (Article 17)

Not just for individual systems, but organisation-wide. Covering the full AI lifecycle: design, development, testing, deployment, monitoring, and decommissioning.

4. A risk management system (Article 9)

Continuous, not one-off. Identifying, analysing, evaluating, and mitigating risks throughout the system’s lifecycle. Including foreseeable misuse scenarios.

5. Data governance measures (Article 10)

Documented data collection, preparation, and validation processes. Bias analysis. Data quality criteria. Representativeness assessment.

6. Human oversight capabilities (Article 14)

Mechanisms for human operators to understand the system’s output, override or reverse decisions, and intervene when needed. For automated credit decisions, this likely means a human review process for edge cases and appeals.

7. Automatic logging (Article 12)

Your high-risk AI system must automatically log events during operation. Logs must enable traceability and monitoring. Deployers must retain logs for at least six months.

8. EU database registration (Article 49)

High-risk AI systems must be registered in the public EU database before being placed on the market or put into service.

9. EU declaration of conformity (Article 47)

A formal document per Annex V, kept for 10 years, declaring that the system meets all applicable requirements. Must be made available to national authorities upon request.

The Penalty Conversation

The EU AI Act has teeth. Real ones. Article 99 sets out a tiered penalty framework:

| Violation Type | Maximum Fine |

|---|---|

| Prohibited AI practices | €35 million or 7% of global annual turnover |

| High-risk AI system violations (your concern) | €15 million or 3% of global annual turnover |

| Providing incorrect information to authorities | €7.5 million or 1% of global annual turnover |

For a bank with €5 billion in annual revenue, 3% is €150 million. That’s not a compliance cost - that’s an existential risk event. And unlike GDPR fines, which took years to materialise after the regulation went live, the EU AI Act enforcement infrastructure is being set up in parallel with the implementation timeline. The European AI Office is already operational. National authorities are being designated.

Will regulators immediately start issuing maximum fines on 3 August 2026? Probably not. But they will start asking for documentation. And if you can’t produce it, you’re in the gap between “technically non-compliant” and “actively being investigated.” Neither is a comfortable place for a regulated financial institution.

Your Month-by-Month Plan (March-August 2026)

Five months. Here’s how I’d spend them.

March 2026: Inventory and classification

Create a complete inventory of every AI system in your organisation. Every model, every algorithm, every automated decision system. Classify each against Annex III. Determine your role: provider or deployer for each system. Identify systems where you may have “substantially modified” a vendor’s AI. This is the foundation - everything else depends on getting this right.

April 2026: QMS and documentation framework

Establish or adapt your quality management system to meet Article 17. Create templates for Annex IV technical documentation. Start with your most critical AI system - the one where non-compliance would have the biggest impact. Assign a dedicated documentation owner for each high-risk system.

May 2026: Documentation sprint

This is the heavy lift. Write (or compile) Annex IV technical documentation for every high-risk system. Conduct risk assessments per Article 9. Document data governance per Article 10. This will take the most effort of any month in the plan. Consider bringing in external support if your team is stretched.

June 2026: Testing and validation

Run (or document completed) testing against predefined metrics. Accuracy, fairness, robustness, performance under edge cases. Ensure human oversight mechanisms are in place and tested. Run a fundamental rights impact assessment where required (Article 27). Document everything.

July 2026: Assessment and declaration

Conduct internal conformity assessments per Annex VI. Issue EU declarations of conformity per Annex V. Register systems in the EU database per Article 49. Set up post-market monitoring processes. Set up incident reporting procedures per Article 62. Review everything with legal counsel.

2 August 2026: Deadline

All high-risk AI provisions are enforceable. Your systems must be compliant, documented, registered, and monitored. Post-market monitoring begins in earnest. Welcome to the new normal.

The Multi-Regulation Problem for Financial Services

Here’s what makes the August 2026 deadline particularly challenging for financial institutions: you’re not just dealing with the AI Act in isolation. Your AI systems are simultaneously subject to:

- DORA (already in effect) - AI systems are ICT assets requiring risk management, resilience testing, and incident reporting

- GDPR - automated decision-making restrictions (Article 22), data subject rights, data protection impact assessments

- Sector-specific regulation - CRD/CRR for banks, Solvency II for insurers, MiFID II for investment firms

- NIS2 - cybersecurity requirements for essential entities (which includes banks)

- EBA/EIOPA/ESMA guidelines - on outsourcing, model risk management, IT and security risk

Your AI credit scoring model doesn’t just need an AI Act conformity assessment. It also needs to be in your DORA Register of Information as an ICT service. It needs a GDPR DPIA. It needs to satisfy EBA guidelines on credit risk models. And it probably needs to comply with national consumer protection rules on automated lending decisions.

Managing this without a system that maps requirements across frameworks is borderline impossible. It’s the reason multi-framework compliance platforms exist - and it’s the specific problem that Venvera was built to solve, supporting 16 regulatory frameworks with cross-framework mapping that shows where a single control satisfies DORA, the AI Act, GDPR, and other regulations simultaneously.

The Real Risk Isn’t the Fine. It’s the Pause.

Everyone focuses on the penalty numbers. €15 million. 3% of turnover. Big, scary numbers. But the actual risk for most financial institutions isn’t the fine - it’s the operational disruption.

Article 16(h) allows market surveillance authorities to require providers to withdraw or recall non-compliant high-risk AI systems from the market. Imagine your credit scoring model being deemed non-compliant and ordered withdrawn. Not fined. Withdrawn. You can’t process loan applications until you fix it. That’s not a regulatory inconvenience. That’s a business continuity event.

Five months sounds like a short time. It is. But it’s enough, if you start now, assign the right people, and approach it systematically rather than hoping for a grace period that may not materialise.

The institutions that treated GDPR’s May 2018 deadline as a real deadline - and prepared accordingly - had a much smoother experience than those that scrambled in the last month. The same will be true for the AI Act. Choose which group you want to be in.

Don’t Let August 2026 Catch You Off Guard

Venvera helps financial institutions manage EU AI Act compliance alongside GDPR, NIS2, DORA, and 9 other frameworks - with cross-regulation mapping, gap analysis, and risk assessments. Starting at €399/month.

Book a Demo →Last updated: March 2026. Timeline based on Regulation (EU) 2024/1689 as published in the Official Journal. Consult the European AI Office and your national authority for the latest guidance.